Unlock Retirement Security with Permanent Life Insurance Cash Value

Discover how permanent life insurance cash value shields retirees from stock market downturns with a proven retirement strategy, growing steadily over time.

8/27/20254 min read

What’s Possible with Permanent Life Insurance for Retirement

If you’re planning for retirement, you’ve likely considered various index funds, possibly a Roth IRA, and maybe even bitcoin. But one asset in particular that is unfortunately over looked is permanent life insurance. Yes, permanent life insurance offers a guaranteed death benefit for life. But the real power is within its cash value, which can serve as a buffer asset to enhance your retirement plan. We created a blog post regarding buffer assets previously, but we are going to dive in and show an actual example of how this can work in your plan using our client Rebecca.

Rebecca’s Implementation of Permanent Life Insurance

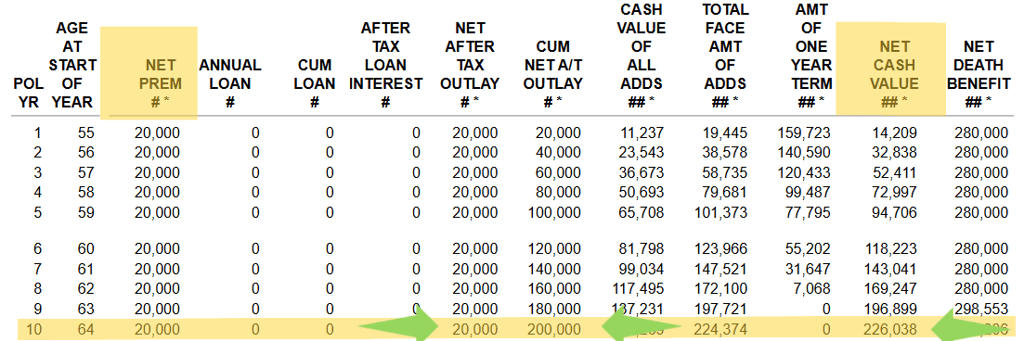

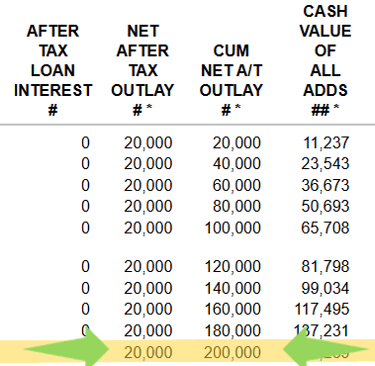

Meet Rebecca, 55 year old Florida native, planning to retire at 65 to maximize her Social Security benefits. She wants to diversify her income and shield her portfolio from stock market corrections. Rebecca needs $100,000 annually in retirement. Her social security is projected to provide $35,000 a year and she has locked in a guaranteed annuity payout of $40,000 a year for life starting at age 65. This leaves Rebecca with a $25,000 annual gap that she will fill with disbursements from the stock market. She understands the stock market has downside risk, but knows long term the market goes up. She wants to avoid selling stocks at a loss in bear markets which ultimately will eat at her account and possibly leave it depleted later on in retirement. So Instead of selling stocks during downturns, she wants to create a buffer asset using permanent life insurance to draw upon during those down turns.

Rebecca commits $20,000 annually for ten years via a 10 pay whole life policy. By year 10, the policy has $226,038 within the cash account after paying in a total of $200,000. The policy earns a 6.10% dividend on the total cash value that compounds year after year tax deferred. So by the time she reaches the age she plans on retiring, she will have paid up the policy, and it will be ready for access when the first market downturn occurs.

Using Cash Value to Navigate Market Downturns

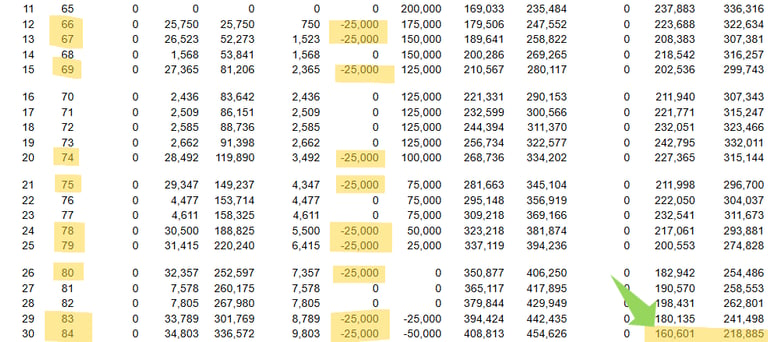

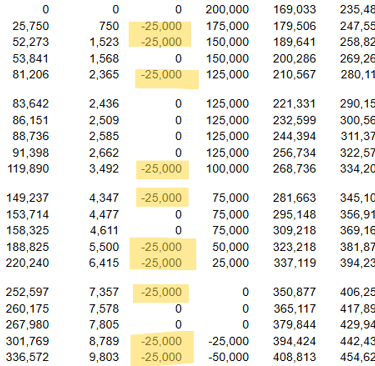

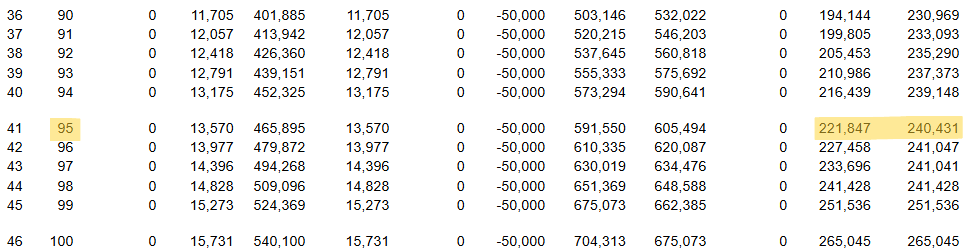

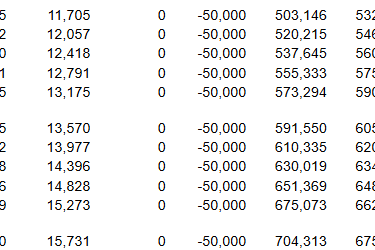

In this example, Rebecca faces 10 market corrections during her retirement, with the first bear market occurring a year after she retires (every retirees worst nightmare). Each year that there is a correction or bear market Rebecca will be withdrawing $25,000 that way she doesn't need to access her investment accounts. From age 66-67, and age 69 she accessed a total of $75,000. Ages 74-75, $50,000. From age 78-80 another $75,000. Finally ages 83-84 access of $50,000 as shown below.

To break it down, she pays $200,000 over 10 years into her policy, loans out $250,000 tax free, and by the age of 95 maintains a cash value of $221,847 and death benefit of $240,431 even though she never paid another dime back into the policy.

Now how is this possible? Because loans within a life insurance policy are not the same as traditional loans. When you take a loan within your policy, the total cash value continues to receive interest, not just the money that has not been loaned out. Think of it like taking out a HELOC. You borrow against the equity of your house, however the real estate continues to appreciate in whole, not just what's left over from what's been borrowed. The same is true with whole life policies. Now how there is positive cash value and death benefit comes down to the interest rate arbitrage. Loans are taken out at 5-5.5%, while all the funds within the cash value, even loaned out funds, received a 6.10% dividend credit. So basically, you are earning interest to take out the loan, which puts you at a net positive.

This approach lets her equities recover, preserving her long-term wealth. She borrows against her cash value, which continues appreciating due to the dividend-loan spread. If she lives to 100, her cash value and death benefit reach $265,045, with $540,000 in loans outstanding, still positive thanks to the policy’s arbitrage. With no mortgage or major expenses later in life, her cash value keeps growing, offering uninterrupted retirement security and ultimately a death benefit to her heirs.

Build Your Retirement Buffer

This strategy protects Rebecca’s retirement portfolio by letting stocks rebound during downturns, a key advantage over traditional withdrawals. Permanent life insurance acts as a non-correlated asset, unaffected by market swings, complementing diversification strategies. Paired with annuities, it ensures steady income, safeguarding her lifestyle against volatility.

Permanent life insurance can transform your retirement plan amid market uncertainty. Review your portfolio to integrate cash value strategies, explore annuities for guaranteed income, and diversify strategically. Consulting an advisor can customize this to your needs. Try our Retirement Income Calculator to see how structured income can compliment your overall retirement plan. Ready to secure your retirement? Schedule a complimentary strategy call today to see how cash value life insurance may fit into your plan.