Should Married Couples Combine or Separate Their Annuities in Retirement?

A South Florida couple planning for retirement wonders if they should open a joint annuity or separate ones. Here’s what to know about the different outcomes.

7/10/20255 min read

Should Married Couples Combine or Separate Their Annuities in Retirement?

For many South Florida couples approaching retirement, a top priority is making sure essential expenses are covered for all of retirement. A lifetime income annuity is a popular way to create a personal pension: a stream of income that you can count on, no matter how long you live. But for couples, an important question arises early in the planning process:

Should we open a joint annuity contract or keep things separate with individual contracts?

The answer isn’t always obvious. It depends on a few key factors, including where the money is coming from and what your goals are. Whether it’s maximizing flexibility, protecting your surviving spouse, or minimizing taxes.

It All Starts With the Source of Funds

Before you choose the structure of your annuity, you’ll need to understand how the money you're using is categorized for tax purposes. That’s because the tax designation of the funds determines whether joint ownership is even an option.

If you're funding the annuity with qualified assets like a 401(k), 403(b), or Traditional IRA, then joint annuity contracts are off the table. These types of accounts are tied to a single person’s tax ID, and the IRS requires that they be kept individual. You can still create a retirement income plan with these funds, but joint ownership won't be part of the strategy.

On the other hand, if the funds are non-qualified such as after-tax savings from a brokerage account or a CD, or savings account, then you have more flexibility. In this case, joint annuity contracts are allowed and often make sense for couples looking for shared lifetime income.

Let’s assume for the sake of this example that the couple is working with non-qualified money, so they have the option of a joint account or an individual account.

The Case for a Joint Annuity Contract

A joint annuity is designed with survivorship in mind. It ensures that income continues for as long as either spouse is alive. This type of setup offers peace of mind, especially in a household where both spouses rely on the annuity income to maintain their lifestyle. If one spouse passes away, the income doesn’t drop or stop, it simply continues for the surviving partner, just as it did before.

This kind of predictability can be incredibly valuable. It simplifies the plan: one contract, one income stream, one set of decisions to make. For many couples, especially those who value long-term security over flexibility, a joint annuity can feel like the obvious choice.

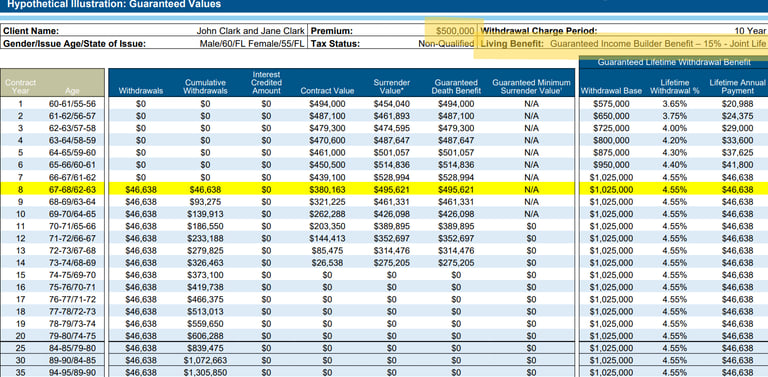

Take a look at the example to visualize how a joint annuity works. A couple John and Jane fund a joint annuity with a shared $500,000. John is 60 years old and wants to work another 8 years because he enjoys his career, and also wants to defer social security to maximize his monthly benefit. Jane is 55 and also enjoys her career. She wants to work for another 12 years until she reaches age 67 to benefit from the full retirement age (FRA) social security benefit amount. Being that John will retire first, they will turn the income switch for their annuity on when he retires to fill his income gap.

When John and Jane turn the income switch on, they will generate $46,638 in income from their annuity. This is guaranteed to last the rest of their lives. Now even If John pre-deceases Jane or the other way around. The income will continue on to the surviving spouse.

The Case for Two Individual Annuity Contracts

On the other hand, each spouse owning their own annuity does introduce some powerful advantages, particularly around timing, control, and income payments.

Imagine the previous scenario again. Jane retires 12 years later at age 67 and John retires 8 years later at age 68. With individual contracts, the spouse who retires first can begin receiving income right away, while the other spouse who is still receiving income from their job allows their annuity to grow until they finally decide to retire. This deferral often leads to a larger payout down the road. In other words, it creates a staggered income strategy that matches real life retirement timelines.

However, there's a trade-off. If one spouse passes away earlier than expected, the income from their annuity stops. Any remaining account value is paid out, but the stream of guaranteed income ends. That’s a key difference compared to the uninterrupted income of a joint contract.

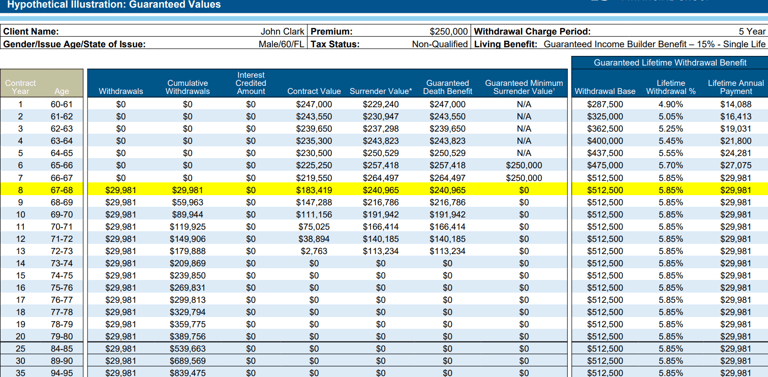

Continuing with the previous example of a couple allocating $500,000 to a joint annuity. Lets say the decide to open their own contracts, John at 60 years old and Jane at 55 years old. John and Jane are retiring in the same timeline as before. John in 8 years, Jane in 12 years. John funds his annuity contract with $250,000. When he turns the income switch for his annuity on 8 years later, he will receive $29,981 per year for the rest of his life.

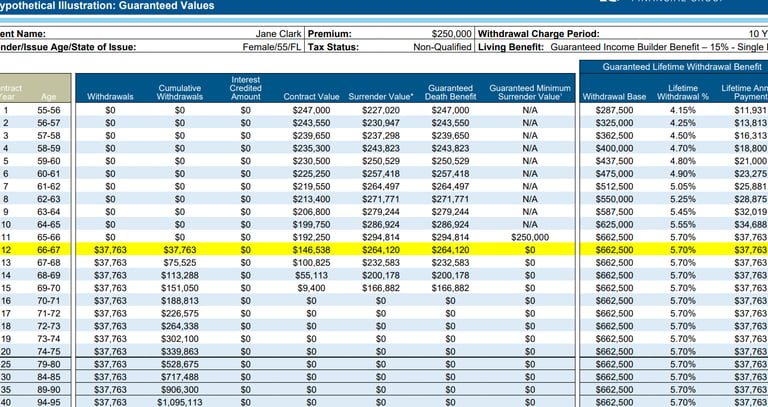

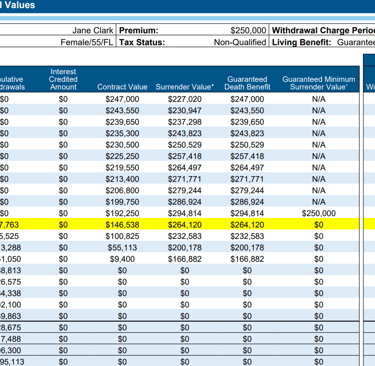

Jane funds her contract with $250,000 as well. However she will defer taking income for 12 years until she retires. When Jane turns the income switch on for her annuity contract she will receive $37,763 per year for the rest of her life.

Once John and Jane both have their income activated the household will be receiving $67,744 a year in guaranteed income. Compare that with the joint annuity paying $46,638 per year, the difference is $21,106 more per year.

Which Option Is Best?

As you can see from the examples above, a joint annuity will have a lower payout then the same amount in two separate annuities. The real trade off is the survivorship income. There's no one size fits all answer. If your top priority is to make sure that income never stops for either of you, a joint annuity may be the best fit. It's straightforward and ensures long term security, especially when using non-qualified funds.

But if you're looking for more control over how and when income is turned on, or if you’re retiring at different times, then separate contracts will offer the flexibility you need. Just keep in mind the risks that come with that flexibility, especially if one spouse passes away early in retirement.

Final Thoughts for South Florida Couples Planning Retirement

Your income strategy should be designed around how you live and how you plan to retire. The good news is, both options can work beautifully with the right plan in place. What matters most is that your income strategy supports your lifestyle, protects your loved ones, and helps you retire with confidence.

If you’re a couple in South Florida exploring annuity options, we can help walk you through side-by-side illustrations to show exactly how each approach might work for you.

Want to see what a joint vs. individual annuity plan could look like for your household?

Schedule a free retirement income review today