Should You Delay Social Security? Pros, Cons, and How Much More You Could Get

Learn the pros and cons of delaying Social Security benefits. Discover how much your monthly income could grow and when it makes sense to claim early or wait.

6/13/20253 min read

Should You Delay Social Security? Here's What You Need to Know

When it comes to retirement, one of the most important and often misunderstood decisions you’ll face is when to start collecting Social Security. You can begin as early as age 62, or wait as long as age 70. But what you choose can significantly impact your monthly income, your lifetime benefits, and even your spouse’s financial well-being.

The decision isn’t as simple as “now or later.” It’s about understanding how the timing affects your income, taxes, and long-term security.

The Case for Delaying Social Security

Delaying your Social Security benefits beyond your Full Retirement Age (FRA) results in a higher monthly payment for life. For every year you wait after your FRA, typically age 66 or 67 depending on your birth year, your benefit increases by approximately 8% per year until age 70.

This growth can make a substantial difference. For example, if your full retirement benefit is $2,000 per month at age 67, waiting until age 70 would increase it to around $2,480 per month. That’s a 24% increase in guaranteed income and inflation-adjusted.

This boost can make a big difference, especially if you’re concerned about outliving your savings. It also means your surviving spouse could receive a larger benefit if you pass away first.

Delaying Social Security is particularly advantageous for those in good health with a longer life expectancy, or for retirees who have other sources of income to bridge the gap in the meantime.

Why Some People Choose to Claim Early

Of course, delaying isn’t the best strategy for everyone. Some people retire early, out of choice or necessity, and need the income immediately. Others have health concerns that may limit their longevity, making it more sensible to begin benefits sooner.

Additionally, some retirees prefer to enjoy their early retirement years while they’re healthiest even if it means smaller monthly checks.

If you claim benefits at age 62, your benefit will be permanently reduced by about 30% compared to what you’d receive at your full retirement age. That’s a big cut, especially if you expect to live into your 80s or 90s.

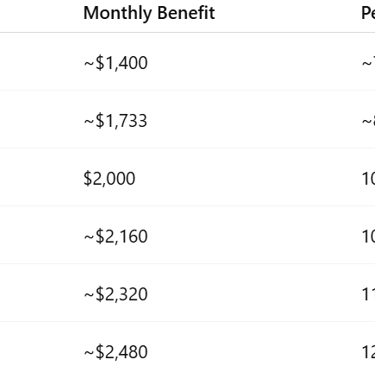

How Much Does Your Benefit Grow If You Wait?

To make the trade-offs more concrete, here’s how your monthly benefit changes depending on when you claim:

Assumes a $2,000 benefit at Full Retirement Age (67).

As you can see, each year you wait provides a guaranteed increase in your benefit. That increase continues to pay off the longer you live.

What’s the Right Strategy for You?

There’s no one-size-fits-all answer. The best time to claim depends on your unique financial picture—your savings, health, retirement goals, and whether you're married.

Some people coordinate Social Security with other income sources, such as annuities or investment withdrawals, using those funds in the early retirement years so they can delay Social Security and maximize their lifetime benefit.

Others might benefit from claiming early and investing the income. However, this approach comes with risk, and the market returns may not outperform the guaranteed growth of delayed benefits.

That’s why we recommend you approach this decision as part of a comprehensive retirement income plan.

Final Thoughts

Deciding when to claim Social Security is one of the most important financial decisions you’ll make in retirement. Claiming too early or waiting too long could cost you tens of thousands of dollars over time.

At LegacyHaven Advisors, we help clients develop smart strategies to turn their savings and Social Security into reliable income. Whether you’re considering retiring soon or just planning ahead, we can help you weigh your options and build a plan that protects your future.

Want Personalized Guidance?

Schedule a complimentary consultation today.