Tax-Free Retirement with an IUL: Is It Real or Just a Dream?

Can an IUL deliver a tax-free retirement? Learn how Indexed Universal Life insurance works, its risks, and whether whole life is a better fit for your financial goals.

7/26/20254 min read

Tax-Free Retirement with an IUL: Reality or Fantasy?

You’ve probably seen the hype on TikTok or online ads touting a tax-free retirement through an Indexed Universal Life (IUL) insurance policy. The pitch is straightforward: a life insurance contract with a cash value account that grows tax-deferred, tracks a market index like the S&P 500, offers growth potential without market losses, and allows tax-free withdrawals through policy loans. It sounds promising, but is it a practical strategy or just a compelling sales pitch? At LegacyHaven Advisors, we’re breaking down how IULs work to help you decide if they can truly deliver a tax-free retirement.

Understanding Indexed Universal Life (IUL) Insurance

An Indexed Universal Life policy is a type of permanent life insurance that pairs the flexibility of universal life with a cash value component linked to a market index, such as the S&P 500. The cash value grows tax-deferred based on the index’s performance, with interest credited up to a cap, often 10-13% with reputable insurers. If the market drops, a 0% floor protects your cash value from losses. You can access this cash value tax free through policy loans. This structure makes IULs an intriguing option for retirement planning, but success depends on how the policy is designed and managed.

The Appeal of a Tax-Free Retirement

The core idea behind using an IUL for retirement is to build a cash value that you can borrow against tax-free later in life. By funding the policy with premiums, you create a pool of money that grows without annual taxes and can be accessed to supplement retirement income. The promise of market-linked growth with downside protection adds to the appeal, suggesting you can benefit from stock market gains without the risk of losses. However, achieving this outcome requires careful planning, and there are pitfalls that can undermine the strategy.

Why Policy Design Matters

The effectiveness of an IUL as a retirement tool hinges on its structure. To maximize cash value growth, the majority of your premium payments should go toward the cash value account rather than the death benefit. For example, if you contribute $20,000 annually, an optimized policy might allocate $18,000 to cash value and $2,000 to the death benefit. Unfortunately, not all agents prioritize this approach. Some, whether due to inexperience or competing incentives, design policies that favor the death benefit, which generates higher commissions but limits cash value growth. This can leave you with a policy that falls short of your retirement goals. At LegacyHaven Advisors, we stress the importance of structuring an IUL for your benefit.

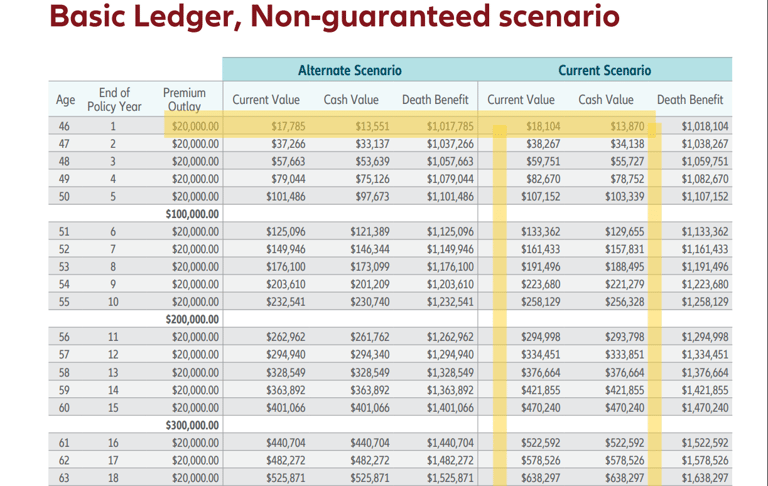

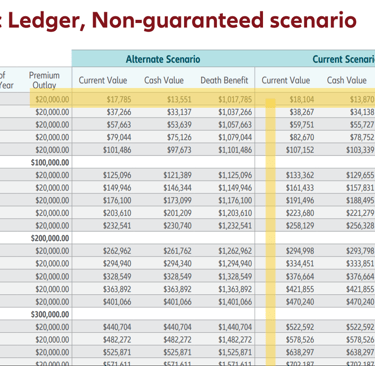

Decoding Policy Illustrations

When you’re presented with an IUL, you’ll likely see an illustration projecting future cash value growth. These projections often assume a steady annual return, such as 7.74% in the example below, which can paint an overly rosy picture. In reality, IUL returns are tied to an index with caps and floors. You might earn up to 10-13% in strong market years, 2-3% in modest years, or 0% when the market declines. The S&P 500 doesn’t deliver consistent returns year after year, so expecting steady growth is unrealistic. Ask your agent for a conservative illustration that reflects market variability to better understand potential outcomes.

Risks to Consider

While IULs offer unique advantages, they’re not a guaranteed solution for a tax-free retirement. Poorly designed policies can result in minimal cash value growth, and high fees—such as premium loads and insurance costs—can eat into returns if not carefully managed. Policy loans also require caution; unpaid loans can accrue interest and potentially cause the policy to lapse, which could trigger taxes. Additionally, IULs don’t provide dividends or other income sources that traditional investments might offer. Misleading projections or mismanaged policies can lead to disappointment, not because IULs are flawed, but because expectations were misaligned.

Whole Life Insurance: A More Predictable Alternative

For those seeking a more stable approach, whole life insurance offers a compelling alternative. Unlike IULs, whole life policies provide guaranteed cash value growth, often enhanced by dividends from top mutual insurance companies. These companies have a track record of paying dividends consistently since the 1800s, through events like the Great Depression and the 2008 financial crisis. Like IULs, whole life allows tax-deferred growth and tax-free access via loans. While growth may be slower than an IUL in strong market years, the predictability makes it a strong choice for conservative investors.

The Role of Diversification

Neither an IUL nor whole life insurance should be the sole pillar of your retirement plan. A balanced portfolio might include market investments for growth, fixed-income products like annuities for reliable income, and tax-advantaged accounts to minimize future taxes. By diversifying, you can balance risk and reward while building a retirement strategy that aligns with your goals.

Conclusion: Reality or Fantasy?

Can an IUL deliver a tax-free retirement? It’s possible, but only with proper design and realistic expectations. A well-structured IUL, crafted by a knowledgeable agent, can provide tax-free income and market-linked growth with downside protection. However, poor design, high fees, or overly optimistic projections can derail the strategy. Whole life insurance offers a more predictable alternative for those prioritizing stability. Ultimately, a tax-free retirement is achievable with careful planning and diversification, but it’s not a one-size-fits-all solution.

Next Steps

Considering an IUL or whole life insurance for your retirement plan? Contact LegacyHaven Advisors for a personalized review of your options. Visit our website or schedule a consultation to build a strategy that aligns with your financial future.